What do most of us have......really really desperately wanted it initially..........but now we really really want to get rid of (a clue, it's not your partner!).................the answer is of course our mortgage!

We have covered mortgages a few times on here, including the ever popular 'should I clear my mortgage or save for the future' episode. This week we are going to ramp up the pressure on existing mortgage holders, we are going to hold a mirror up to them and their habit, and indeed inertia! In a survey we held earlier this year we asked how many of you believed you were on the best possibly mortgage rate.....interestingly 70% of people were not sure!

That points to the fact that people aren't informed as to the best mortgage rates in Ireland at the moment, and whether they are getting the best deal available or not.....we are going to fix that right now! Switching mortgage in Ireland for some reason is no that popular versus many other states, however for some it can be a very financial prudent thing to do!

Firstly, thanks for checking out Ireland's #1 Financial Planning Blog & Podcast, we are delighted to have you visit! By all means please do check out our 'why' which will explain why we are creating this blog and podcast every week for our listeners and readers! Also, thanks a mill' to our latest iTunes Reviewer, it means a lot to us, so please do pop over and leave a review if you have a minute!?

Can I Switch My Mortgage?

There's no point in getting all excited about the benefits of switching mortgage (there can be many!), if it is not available to you....here's what you'll need to prove:

- You have an existing mortgage!

- You live there (usually only benefits 'owner-occupiers)

- You have a clean payment history on that mortgage in recent years

- You have consistent/permanent income(s) which the bank will deem sufficient to repay the 'switched' mortgage

- You have the time required to compile documentation & attend solicitor and bank/broker in order to switch to the new loan

- You will want to be benefiting financially in order to even consider switching, so you'll need to know what the savings (if any) will be

- Be prepared for some element of hassle, as these things usually always have some twists and turns!

- You will need to be of an age where the bank is willing to give you the new mortgage up to a reasonable age, some banks will lend to you till you are 65, others to 70.

Should I Switch My Mortgage?

Another humdinger of a question! We can't answer that question for you, but we can show you how to answer it for yourself. There are lots of comparison websites in this country, and there is no doubt that they help people get better deals. They make their money from people switching. There is also a government funded switching site that is pretty awesome, which we are big fans of here, and that is the Competition & Consumer Protection Commission website (I think they could do with some help on the name of the site in fairness!). It's a fabulous and totally un-biased site which is updated daily.....check it out here.

All you need to have to hand in order to do a comparison is the following:

- How many years left on your mortgage

- Approx value of your house

- How much you owe currently on the morgage

- How much you are paying each month

Be careful with number 4. Make sure that the figure you put into the calculator is the amount you are paying toward the mortgage each month. So of us have home insurance or mortgage protection included in the same direct debit. Make a phone call to your lender if needed in order to determine exactly how much the mortgage repayment is on it's own.

Whack the figures into the calculator and select whether you want to compare it to best Variable rates, or Fixed rates of the various terms 1 year to 10 year.

What is APRC?

In the next section you will see APRC referred to when detailing two different rates of interest on a mortgage. This stands for Annual Percentage Rate of Charge (as if we needed another acronym!). It is however the only accurate way to compare two rates as it includes all charges in the rate, including set up charges. It is common to see an interest rate quoted of say 3%, however the APRC is almost a full 1% (3.9%)......moral of the story is that you go with the APRC in comparing loan rates......now that we have that cleared up lets get on with the story for you....

How Much Could I Save By Switching Mortgage? A real-life story!

We want to share a real-life story with you. A friend of the show, we'll call him Jimmy, got in touch to tell us that on the back of a recent blog/podcast we did he went on the hunt to reduce his mortgage payment. He shared his story with us, and invited us to share it with other listeners so that they could too benefit from it.

Jimmy lived in his house with his wee family. The house was valued at around €290k. He had a mortgage of €170k, and was paying €915 per month. The rate was 3.9%. There were 25 years left on the mortgage. Jimmy and his partner are in their 30's.

They shopped around for the best rate mortgage they could find. They managed to find a market leading fixed rate of 3.05%, for a 10 year fixed mortgage. They were keen to fix it for the medium to long term as they wanted that security knowing it would not increase in future, that was important to them. This rate was subject to them switching their current account, which they were happy to do.

In addition they were going to get 3% Cash-Back provided the loan was drawn-down before March 2018. They were both working and earning the same salaries as when they originally took out the mortgage, with a clean payment history.

They got the ball rolling on the new loan via a broker, informed the original lender of their plans, and then followed the process with the new lender. Essentially the new loan goes directly across to clear the old loan, one cancelling out and replacing the other.

They are now paying €90 per month less than they were on the old rate, with the term the same as the original mortgage (they had the option of reducing the term but they wanted to keep it as long as possible for now). They also got €5,000 Cash-Back recently which has helped them hugely! All complete in a little under 3 months! yes they had to pay a solicitor €1,200 for the legal side of things, and there was some time invested in meetings and gathering info, however.....

Over the term of the mortgage this switch, including the Cash-Back, stands to benefit them €32,000! Delighted for them!

What About The Insurances?

When switching do try and keep your existing Mortgage Life Cover, provided it is the most appropriate cover for you (worth taking this opportunity to make sure it is actually!). Your original lender would need to 'release interest' in the policy before the new lender can note it on the new loan ('assign it'). It is always prudent to make sure it is 'assigned' to the new loan so that in the event of a death the benefit goes directly to the lender to clear the loan.

Also really important obviously to make sure there are no 'gaps' in cover if you are cancelling or replacing either the Mortgage Life Cover or the Home Insurance.....if something tragic were to happen during that 'gap' you could be left in dire straits!

Are There Another Other Options?

Your existing lender might well be able to do you a better deal than you currently have! You may not need to switch lender in order to get a better mortgage deal, saving you the time, hassle and expense which comes from moving to the new lender (documentation, solicitor fees etc). So if you have decided to switch it is always worthwhile contacting your current lender and telling them your gone unless they can do something similar for you!

So there you have it.......the 'can I', 'should I', 'how do I', 'what will I save' of the mortgage switch conversation.....do be a legend and share this with your peers and anyone who you reckong would benefit from knowing about this.

Thanks for reading, you're a legend!

Paddy Delaney

QFA | RPA | APA | Qualified Coach

Welcome to another episode of Ireland's #1 Financial Planning Blog & Podcast.

This week we have a cracking interview with UK's Jason Butler, where we discover some tips and guidance on achieving financial well-being, getting our lives the way we want them to be.

Jason has super insight on this aspect of life, and is now living his message.......most of us will hopefully take a few nuggets from this interview (I'm not taking any credit there!).

Be sure to check out our wee website, our why, and if you like the show then an iTunes review would be a much appreciated gesture to us.......You're a legend!

Enjoy,

Paddy Delaney

QFA | RPA | APA | Qualified Coach

This week we are aiming to share some slightly different insights, and reveal some major news in the world of Financial Services in Ireland! Last week the Central Bank released a proposal which is due to come into force next year (subject to Dept. of Finance), which is aimed at maximising the protection consumers get when it comes to buying any financial products....we have dissected all the Publications released by Central Bank to determine the details, and it's an interesting one!

Firstly, thanks for checking out Ireland's award-winning Financial Planning Blog & Podcast, we're delighted to have you join us. We'd be thrilled if you had the time to check out our 'why', and to learn a little about what we are trying to do, for you our reader.

The Green-Grocer!

Indulge us for a few moments, trust me it'll make sense shortly! Imagine that you are walking down the road after getting off your bus from work, and you notice a shiny new green-grocer shop on the corner. It's called 'Gerry's Independent Stores'...sounds good to you!

You walk in and the friendly green-grocer welcomes you with a big smile, a warm welcome, and inquires as to how he can help you.....you are taken aback at his hospitality and part of you reckons 'I'm gonna be sold something here'....therefore you reply in the usual way and state that you are 'just in for a look'!

The shelves are stacked high with produce, so much choice of all your staple items, different versions of everything......you are confused with the level of options and so ask for some help with regards picking the 8 items you actually do need, milk, bread, broccoli, ham, cheese, yoghurt, apples & grapes (you healthy divil you!).

Before you know it the kind shop keeper picks out a version of each of the 8 items, in addition he tells you that he has a special rate going on the eggs, asparagus, Mars Bars, and Ice-Cream and he encourages you to buy those as well. You reckon that you actually probably could use these other items so you agree to buy them.

You go to the counter, pay for your stuff and happily head on off home with your shopping for the next few days done, and away home to make the dinner!

How Did The Green Grocer get Paid?

It is only the next day that you hear from a mate that the Green-Grocer actually makes more profit on certain options than on others. He picked the options for you that result in him getting the most profit. He also invited you to buy more stuff, because it turns out he gets a large bonus from the provider of the eggs, asparagus, Mars Bars and Ice-Cream if he sells a certain amount of it. In fact, he actually also get a holiday every year if he sells certain amounts of it to his customers. He might also actually get support to pay for advertising and marketing if he agrees to only sell that particular producers product....how do you feel now? Some people might feel like that is what they expect, others might not care less, while others might feel that they were being encouraged to take and buy stuff that might not have been the things that they needed or wanted! Again, how would you feel?

How Are Financial Advisors Paid?

It will be no surprise to majority of you to hear that most Financial Advisors & Intermediaries, Banks, Brokers are paid in a similar way. Majority of Brokers, Banks & Advisors (also known as Intermediaries- i.e the seller of products on behalf of a product producer) get paid commission when they sell a certain product. It is also known that some get paid more for selling a certain product, and indeed get paid bonuses if they sell a certain amount of certain products from certain providers....all very certain!!

It appears to us that the Central Bank are on a mission to increase the transparency that you the consumer has in regards how your 'Green-Grocer' is paid by the providers. In fairness that makes total sense. As we keep banging-on-about here, the focus of the industry has for too long been lazered onto selling products as opposed to delivering the real outcomes that consumers need and want....more often than not a product is required, but it should not be the starting point of the conversation!

What Will Change For You, The Customer?

In essence what the Central Bank appear to be aiming towards is a situation where there is a full and clear menu available to the customer as soon as they look up the 'Green-Grocer' online....you the customer will be able to see exactly what the grocer is paid from each provider, in advance of you actually going into the shop.

The impact of this would be that the next time you go into 'Gerry's Independent Stores' you will know how much Gerry will make if he sells Brocolli A, Brocolli B, or Brocolli C.....again all about improving the transparency for the shopper.

Also, when it comes to mortgages, the Green-Grocer is currently paid a % of the loan that the customer takes out (Green-Grocer being bank/broker/any intermediary), so the more you borrow the more commission the grocer gets.....well they are looking to put an end to that it seems, by introducing a cap on commission which the grocer gets, irrespective of the amount being borrowed....again our take is that The Central Bank are aiming to reduce the chance of a consumer being 'given' more of a loan than they need, which would mean that the grocer gets a bigger commission. Them days appear to be at an end.

Is Gerry Independent??

As you have heard, Gerry's store is called 'Gerry's Independent Stores'......however if you are looking at how he is getting paid and the bonuses he can make by selling more product from a certain provider etc, then you could argue that he is not independent!

If the Central Bank's recommendations come into force in full next year Gerry will have to remove 'independent' from his store name! The Central Bank appear to be very keen to ensure that only a grocer who is receiving no form of commission from a provider can class themselves as independent. Meaning if you go to an independent store once these recommendations come into force that you will have to pay out of your own pocket for the advice and recommendations. If they do state that they are not chargin you commission but that they are charging you a fee, which is being paid to them out of your products, via the provider, this will be classed as not being independent from the provider, and hence not independent in nature.

How Can I Get Independent Financial Advice in Ireland?

In simpler terms only a grocer who does not take commission of any sort, whose only income is the income he or she gets from charging a fee directly to the customer, will be able to call themselves independent under the new Central Bank recommendations. That is quite different to what is and isn't classed as independent in today's world of financial advice! If you think about it it makes lots of sense to only allow an advisor who is totally, financially and otherwise, independent of the product provider to be able to call themselves independent......

How Will This Impact On Us Getting Financial Advice?

Some are saying that it might reduce the number of financial advisors in the country. Others are saying that financial advisors who typically have lots of providers to choose from will reduce the number of providers to just 1, so as to remove the need to choose between different ones based on something other than the commission. Others say that it will open consumers eyes to the level of commissions that are being paid, and will disillusion them about financial advice altogether.

The last point, from our perspective would be a huge shame. The benefit of true financial advice and financial planning is usually way way beyond the cost associated with it. The avoidance of huge mistakes, the putting in place of plans which support your long term goals and lifestyle aims is worth so much more than the cost, again usually! We, for what it is worth, hope that the impact will be the rise of much more customer focused approaches from more and more of the industry. If that happens, and much like the investment markets nobody knows, then the recommendations will have been a rampant success.

We're hoping.

Thanks for reading.

Paddy Delaney

QFA | RPA | APA | Qualified Coach

Welcome to Ireland's #1 Financial Planning Blog & Podcast. Our purpose is to help you make informed decisions with your money, and importantly to avoid some costly mistakes that they rest of us have made! We are aiming to make this THE home of Financial Planning ideas and insight for normal people in Ireland!

This week, after last weeks' cracker about clearing your loans at 32, we are back with a bang, and what more do we love than a good oul list! Which is ironic seeing as only recently I had the fortune to have attended a Workshop on using Mind-Maps....which suggest that lists are the devil's work and that our brains hate lists really. I have to say I am a fan of Mind-Maps now, I'm converted, so don't be surprised if I land a financial one on you all in the very near future!

It was actually doing a Mind-Map for myself that got me thinking about what is absolutely of most importance to me at the moment in terms of personal, family, career etc. It got me thinking of what we might say to an 18 year old version of ourselves, had we the chance to go back and give ourselves a right good talking to!! So here's my take on the 5 Simple Things I would encourage myself to have done financially from that age:

Be A Life-Time Learner: Personally I'm a little late to this party, only really getting into 'informational sponge' mode in the past 5 years. Had we forced ourselves as 18 year old's to read, and be curious about all things financial it probably fair to say we would be in a much better position financially than we are currently. So if you have found that you are still a little financially illiterate (you couldn't be if you are reading this right!!) then may I suggest starting with this book, a true gem; Millionaire Teacher.

Harness The Power Of Compounding: We have flogged this one to bits here at Informed Decisions but there is absolutely no escaping what Einstein referred to as the 8th wonder of the world. Imagine starting off at 18 years of age saving €250 per month. If you achieved a growth of 6% per annum, by the time you are 48 years of age this is worth €250,000, you yourself contributed a mere €90,000, the rest, €140,000 was magiced-up via compound interest....what possibly are you waiting for dear friend!

Become An Owner As Early As Possible: We believe that owning is much much more advantageous than borrowing. Take a home, for most us we need to be a borrower before we can be an owner.....the earlier you borrow the earlier you own (clear the friggin mortgage!). Despite the ups and downs of property value it is quite often clear to see that the sooner you can get onto that ladder, barring disaster, you may well stand to benefit earlier. The very same can be said of owning investment assets, be they property, equities, or other, it is much better from a long term returns perspective, to own as opposed to borrow, which you essentially are doing by owning Deposits Accounts!

Spend What You Have Left After Saving: Another that we beat the drum about here. Nobody enjoys the process of actually delaying gratification (usually!). Why would I save this money when I can out on the town tonight with my pals and have a whale of a time!?! By removing this choice from our hands we are ensuring that while still enjoying enough nights-out, that we also squirrel some money aside to realise our goals in the future, whatever they may be. It is so easy now to set up standing orders and savings accounts online that there is really no excuse not to, right now, go and set up a standing order out of your current account and into a savings account, the day after pay-day! Again, what oh what are you waiting for dear friend!? Most of the time people find that they can adapt to the new spending amount, so it's a win-win! And while you are at it I'd also make sure to know exactly what is coming in and what is going out each month....and to turn up or down the savings element whenever the situation warranted it...the art of budgeting!

Keep An Eye On The Small Print: So many people are swamped with jargon and terms and conditions when they do anything remotely financial related. Unfortunately it is usually one EU regulation or another that is insisting that you get this stuff. However the providers of these materials don't always make it easy for you to understand and digest them. One of the biggest culprits here is the fees and charges that you may be paying on financial products, savings, pensions, investments. These fees vary so so wildly from provider to provider that the difference between one and another can be a staggering amount of money.......make sure that that difference is in your pocket. Always always, as painful as it might be make every effort to know exactly what the fees are before you enter into anything......if you can't bring yourself to do it then ask someone for help!

So there you have it.....our 5 Simple Things....Simple but not necessarily easy....but hey nothing worthwhile is easy right!? However with a bit of knowledge and some good old fashioned effort we believe they are realistic, timely and above all hugely impactful for anyone to apply. You might want to send this or share it with someone who could do with the nudge!

Oh, and we are going to be introducing an element of 'readers & listeners questions' on the show every few weeks, so if you have any question you would like answered on the show just pop me an email here and I will do my utmost to include it in the next weeks' show and to answer it coherently!!

Thanks a mill for reading.......

Paddy Delaney

QFA | RPA | APA | Qualified Coach

Welcome to Ireland's #1 Finance Blog & Podcast. We are here to help you make informed decisions with your money...and ultimately to bring true Financial Planning to Ireland's normal people!

This week we are taking a little peep into the magical world of Jimmy & Aggie.....how they have different views on life and money, and ultimately how they went their separate ways with regards their pension options, and how that panned out for each of them!

Aggie's Story:

Aggie is in her mid-30's, a sound woman by all accounts! She works as an Accountant in a medium sized law firm. She's as happy as a trout in her job, and plans on working her way up the ladder over the next 10 years in the firm. Good on Aggie! When she met her now husband Jimmy it was like a scene from a Disney Movie.....sparks were flying.....they were married within 6 months. That was 7 years ago now, and in fairness their gut feeling was right...they're having a ball!

Herself and her husband Jimmy have a wee baby girl, Jacinta, who is the centre of their universe at the minute! Even before Jacinta's arrival Jimmy had been at Aggie to start stashing some of her disposable income instead of spending it on more 'bloody cycling gear' (they are big cycle fans ya know!).

Being the loving and responsible sort she has given in to Jimmy's insistence and recently went to get some advice on getting herself a pension. Aside from Jimmy giving her the verbals about doing it she has read and noticed lots of articles and blogs about it over the last few years, generally scare-mongering her into doing one with headlines such as 'start a pension of die a penniless and miserable oul widow'...none of which really gave her the nudge to do one!

She met with an advisor, a highly qualified professional, also in her 30's. This advisor recommended that she should put in place the 'life-styling' option, which she was told will gradually move her funds from the 'volatile shares portion' of her pension pot to the 'more stable bonds & cash funds' as she gets nearer to retirement.

She is told that by the time she is 65 or so that 75% of the pot will be in 'steady and secure' cash while the other half will be in 'volatile shares'. Ultimately the intention would be to protect the hard earned savings that Aggie would have built up by that stage.

This sounds like a great idea to Aggie, she has heard one or two stories over the years of people 'losing' their pension pot as they get near retiring because of a crash or recession & she ain't a fan of that happening to her thanks very much!

Seeing this as sound advice Aggie duly accepts the recommendation and signs-up, starting off with a monthly payment of €300 to her PRSA. Based on the information that her advisor gave her when she gets to age 68 this should build up to about €200,000 after charges and accounting for the Lifestyling. As a result of reducing the % of your pot invested in funds which offer solid growth, it reduces your potential growth over time.

Fast forward 3o-odd years, Aggie and Jimmy are still blissfully married, their now 3 kids have grown up and left the nest educated and set up to go and do their thing! They are both eagerly anticipating their retirement and going to do all the things that they have been putting off for 30 years (you can see where this is going!!). Aggie has long dreamed of herself and Jimmy taking 6 months to cycle across America......a friend of hers did it a decade ago and she has been planning for it since. She reckons that trip alone is going to cost them in the region of €30,000, a fair chunk of her anticipated €50,000 tax free lump sum from her PRSA when she retires.

As luck would have it just as Aggie is turning 68 and about to cash in her pension pot the markets have a shocker.....a global financial crisis of 2007 proportions strikes....global equities fell in value by 50%. Luckily for Aggie only 10% of her total pension pot (€200,000) was sitting in an equity fund. It could have been an awful lot worse but because the bulk of her fund was in cash her fund value has only fallen by €10,000, from €200k to €190k, as she goes to retire.

At this point in time she is showering grateful blessings on the advisor she met all those years ago for recommending Life-styling. Had she not had Life-Styling she would have potentially still been fully invested in Equities, and therefore lost half of her total pot.

Aggie then takes her 25% tax free lump sum, squirrels the rest into an Approved Retirement Fund (Check this out if that means nothing to you!). With her €47k tax free lump sum she decides then to treat herself and Jimmy to a 1st class trip via Concorde (its 2058 now, Concorde has been reintroduced right!!) to the west coast of USA to begin their cycling adventures.....the rest is history!

On her return from the trip she decides to leave the fund 100% in 'safe' funds which offer no potential for growth but at the same time won't fall in value.....

So Life-Styling did a great job for Aggie here, it saved her large cash-pile of €200k falling in value by a full half just as she was going to retire.

So What Were The Benefits & Not-So-Benefits Of Life-Styling On Her Pension?

- It protected her fund from falling sharply in value as she was retiring (cashing it in)

- It gave her peace of mind knowing that the funds were being 'de-risked' as time went by

- It reduced the potential for growth in her pension pot as time went by

- If she stays in these low volatility funds she will likely be losing money versus inflation over the course of her retired years.

- She will be paying fees to be in funds which are unlikely to earn any real return for her

So Let's Now Hear Jimmy's Story!

Jimmy was always smart with his money, he was reared with a prudent approach to looking after his money and was a diligent saver from early on in his career. When he set up his pension in his early 20's Jimmy decided to let the constant upward curve of the great companies of the world do their positive thing to his pension pot over the long term, and hence he decided to forego the Life-Styling option on his pension pot. He wanted to leave his funds exposed to the full power of a global equity fund over the long term. He was aware of the fact that volatility is your friend over the long term and so did not want to move the bulk of his money into cash funds as he got older.

Jimmy has been saving €300 into his PRSA since aged 25. Assuming the same annual growth rate as above, however this time without the impact of Life-Styling removing the potential benefit of growth, he will achieve a fund of €540k at age 68. (the power of starting early!!).

Like Aggie Jimmy is mad into the cycling. Loves it, however he doesn't buy all the gear, he rides a 10 year old bike, wears the same 3 bib tights and top for the past 5 years, and services his bike once a year himself.....the ultimate prudent cyclist...he prefers to enjoy his holidays, experiences, and saves the rest...hence his saucy pension pot going on!

As with Aggie lets fast forward 30 years. Jimmy's pot is worth a smoking hot €540k and he is licking his lips at the thought of the big 25% tax free lump sum of €135k.....and again because he is so prudent he is letting Aggie pay for the big US cycling trip...this money is to last him for another 30 years hopefully!

But of course, as you already are aware he suffers the same crash as Aggie (it's the same time of course!). Aggie's fund was well protected from the crash and the 50% equity fund falls however his wasn't, he was 100% in global equity fund, so you guessed it his fund falls from €540k to €270k, yikes! Just as well Aggie is taking care of the US trip.

So what does Jimmy do now? Well he has options....he can leave the funds there and let them recover. And here is the kicker ladies and gentlemen............the average period of time it takes the market to go from 'very bottom' (trough) to 'very top' (peak) over the last 23 bull/bear market cycles has been 1096 days, less than 3 years (based on our own calculations from Standard & Poors Corporation data).

This suggests that if Jimmy leaves the fund alone and lets Aggie look after things for a few years his €540k will be restored in full....and he can then go about taking his tax free lump sum and invest in his ARF/AMRF, and yes still continue to invest in the constant upward curve of the great companies of the world...happy days! Yes for sure it would have been a challenging time and one in which he would have had to resist the temptation to move his pot out of the rapidly declining equity funds and into the 'secure' cash fund, but that would have been the singly most financially costly mistake he would have made over his entire life, fact. Well done Jimmy for not doing that, for trusting the upward curve and for remaining optimistic.

The Benefits & Not-So-Benefits Of Not Having Life-Styling On His Pension?

- It allowed his fund remain fully invested in the great companies of the world, accessing the growth they achieve over long term (good)

- Allowing him move from working to retirement and the bulk of the funds remain in the same funds (good)

- If the markets took longer to recover then he might need to access the funds, ultimately selling them at a low price (not good!)

- He is exposed to the volatility, and the concern that that can cause an investor (not good if you can't handle it!)

- He is avoiding having to pay high fees for investing in cash funds (which will cost him lots!)

So what's the moral of the story? Should I use Life-Styling on my pension funds? Should I remain invested in what are deemed to be high risk funds in my pension? Is Life-Styling a genuinely useful element on my pension and as part of my overall Financial Planning here in Ireland?

It really depends on your outlook, and on your capacity to ride the crash(es) when it/they hit. If you can do that then perhaps Life-Styling serves little of no purpose for you. In fact Life-Styling, while reducing your volatility as you approach retirement will potentially rob you of much of the gains to be had by investing in the first place....not forgetting that you will be paying in the region of 1-to-2% in fees each year just to be in the PRSA...so if you aren't achieving at least that then you will be losing money anyway- never mind also beating inflation over the long term! To do all that you could be needing to earn in the region of 4% growth per year to thread water!

As always we believe those who work with a competent and effective financial advisor/coach can do it most effectively, can resist the urge to make knee-jerk decisions based on temporary declines in equity values....in the history of the market all declines have been temporary, and that's another fact!

So if you plan to embark on an adventure of a life-time like Aggie & Jimmy did then make sure you know what number your current pension is likely to give you, and if Life-Styling is something which you believe will aid you or hinder you in getting to enjoy that adventure.

Thanks so much for reading.

Paddy Delaney

QFA | RPA | APA | Qualified Coach

P.S: Thanks so much to Devined5 for our latest iTunes Review.......he/she called it a 'super informative investment podcast'.............thanks so much Devined5. If you would like to support us then an iTunes Review is a great way to do so....just follow this link

This week we are chuffed to share with you the story of the guys at '2 Cup House' in USA. They were living the life of modern trappings, and one day decided that they wanted a different route.

It may not be for everyone but it is a great story that proves if you want to achieve something, and are willing to apply yourself if is often very achievable!

As promised in the episode there are a few snaps below of what their home looks like, and here's a link to their Blog.

Hope you enjoy the show, we certainly did!

Thanks,

Paddy Delaney

QFA | RPA | APA | Qualified Coach

This week we will take a look at the empty promise that we hear so many people make to themselves and to their loved-ones! This empty promise is akin to playing Russian Roulette with your loved-ones' financial well-being.....if you are a selfish gambler then perhaps its OK, for the rest of us it simply isn't, no matter what hat we're wearing!

What in the blue-blazes are we talking about? We are talking about the gamble we hear so often, whereby a couple are taking out a new mortgage, and when faced with whether to put in place just the Mortgage Protection, or to comprehensively cover themselves by taking Mortgage Protection as well as an element of Personal Life Cover. Many many people make the empty promise when they say "We'll do the Mortgage Protection now, and sure we'll do some sort of personal Life Cover once things settle down".....that is a "I'm happy to gamble with my families financial well-being" if ever we heard one!!

In this episode we are going to initially look at the basics of the two types of cover....just so we're all on the same hymn sheet! In a few minutes we'll then dissect the merit of the advice to pay for both Mortgage Protection & Life Cover. We'll uncover if having both is as useless as a chocolate fireguard, or if it is actually a prudent and necessary approach to take when it comes to protecting your yourself and your family, and indeed your financial plans here in Ireland.

Firstly, and as always, we are chuffed that you have checked out our award winning Irish Financial Planning & Money Management blog & podcast. We are on a mission to make financial planning accessible to Ireland's millennials! We ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

Welcome to our 61st edition of the informed Decisions Financial Planning Blog & Podcast. Did we mention we were recently voted Ireland's best?? Yes, we are Ireland's #1 Finance Blog & Podcast...!

To celebrate our 61st Podcast we are joined by the one and only Emma Kennedy, journalist & up to recently Editor of Money section in Sunday Business Post.

We get to explore Emma's thoughts and experience in regards lots of topics, Kids & Money, Mortgages, Pension Reforms and the make up of Financial Planning services in Ireland as of today.

We do hope you enjoy this episode, we certainly did enjoy creating it! If you have any questions please do drop us an email, and if you really do enjoy the show we'd be hugely grateful of an iTunes Review!!

Thanks so much for checking this out.

Paddy Delaney

QFA | RPA | APA | Qualified Coach

Two lads were standing at the bar of a Friday night in October....their kids put to bed, they gather for their monthly 'Fischers Friday' in their local pub!

Lad #1: "Hey, they're telling me I should do this AVC pension in work"

Lad #2: "Whats an AVC?? Sure do you not have a pension already in work?"

Lad #1: "Eh, yeah I do yeah but yer one said I should set up this other one to give me more of a lump sum in 20 years!"

Lad #2: "Sure jaysus you could be dead in 2, whats the point in doing an ABC or AVC or whatever it's called?!"

Lad #1: "Yeah but she said that if I don't do it i'll miss out on a load of tax reliefs or somethin"

Lad #2: "Tax relief me eye, sure if you put it all into the ABC thing you'd not be able to afford these pints your about to buy!"

Lad #1: "Ha! But yer right, sure yer one was only trying to sell me stuff I suppose"

Lad #2: "Damn right she was, them ones are all the same, pushy pushy, only interested in themselves, ya may tell her to shove her ABCs!"

This wasn't our attempt at a Roddy Doyle sketch, moreso our interpretation of what we believe probably crosses people's minds when they are invited to look at AVCs! They might not verbalise it but they probably think it.....and to a degree they wouldn't be totally wrong!

This week we were contacted by one of the national papers for our comments on AVCs; the pros and cons as it were. We gladly gave our views, and though it wasn't on the agenda this week we decided to do a piece on AVCs.......it's over-due in fairness! We are hoping to dig into the ABCs of AVCs a little, keeping it simple and looking at it slightly differently, as we do!

Firstly, and as always, we are chuffed that you have checked out our award winning Irish Financial Planning & Money Management blog & podcast. We are on a mission to make financial planning accessible to Ireland's millennials! We ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

So how about we look at that wee conversation above and take it line by line, figure out how right or no they are! Before we begin, in order for an AVC to be of any appeal to you, you need to have A) an understanding of what it is B) clarity on how it will benefit you (or not) in the long term & C) the disposable cash to put into it!.............................................www.informeddecisions.ie/podcast59

OK, we were being a bit mischievous in calling it 'owning'.....but if you have one you'll know that the responsibility lies squarely on your shoulders.....so you may as well 'own' the little darling!! We are not just gonna list off the usual baby stuff, as we like to do here we are going to invite you to think about it a little differently! There are stats which say it costs €250k to raise a child. We're gonna bust through that and break it down a bit more practically!

Many of our readers have kids, and indeed a lot do not, yet! In this episode we are hoping to give some bit of insight to readers on what can be expected financially when you are expecting & beyond.....

This episode is a major departure from the last few weeks where we focused on investment rebalancing, investment portfolios and the impact of time on your investment success. So if it doesn't hit the mark for you then please let us know!! Feedback is gold!

Firstly, and as always, we are chuffed that you have checked out our website & podcast. We are on a mission to make financial planning accessible to Ireland's normal folk in their 20s & 30s (millennials!?). We ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

This episode does not address the costs of trying to conceive and the various medical methods to do that. While this is something which is faced by many many couples, we empathise however we really don't know enough about it here to put together helpful information.

Intro:

So if you are expecting or indeed planning on expecting a wee baby and are wondering how much does it costs to have a child, you are a planful individual! We reckon it is useful to approach this question through 3 different 'trimesters' (like what I did there!?).....the short, medium & the long term.

The short term expenses include everything in the run-up and indeed the first year or so of the child's glorious existence, medium term is from year 1 to year 5, while the long term is everything after that! Let's take a quick look at the main costs of having a baby, on the short term.....

The Short Term:

You don't need us to inform you that there are costs associated with having a baby even before he or she gets here! Here's a broad summary of what you'll be looking at!

Medical Costs: Ranging from €3k to €5k if you decide to use the 'Private' maternity service in your chosen hospital. If you decide to go 'Semi-Private' it will be in the €1k to €2k region, while if you decide to go 'Public' you'll be getting it for all but free. The decision as to which route to go is a very personal one, and in most cases doesn't come down to cost anyway!

There's not too many mammies who would be happy to let a baby arrive home without having all the necessary accouterments! So broadly speaking here's a broad tally of the main bits needed;

Cot/Crib/Changer: €300-€1000

Clothing/Blankets: €200-€500

Buggy/Car Seat ('Travel System'!): €300-€1500

Breast or Bottle Fed: €0- €600

That quick scan (pardon the pun) of the short term costs tells us that you'll need to prepare for spending anywhere in the region of €800 to €8,500, depending on your preferences....and indeed on how many 2nd hand donations you are willing to accept from friends and family (a great source of stuff in fairness!).

Medium Term (1-5 years old):

So baby is home and settled at this stage, and is starting to crawl/walk and give you back-chat! Happy-Days!

As a responsible parent your instincts will likely kick in and make you notice the advertisements and media articles, forcing you to consider such things are making sure you have proper financial protection & provision if 'anything happens' you!

Emergency Fund:

This nugget has been covered umpteen times in fairness. We even covered it way back here in our 3rd blog post. You may already have one in place, but if you don't it can seem a really daunting mountain to climb....to have a stash of cash equivelant to 3-12 months take-home income. So if you are taking home €3,500 per month, you could be aiming to have €10-€40k of a stash! That's no mean feat but the comfort and peace of mind knowing it's there (or at least is being built) is massive. Follow the suggestions here and you should be OK on this front.

You'll Wanna Be Protected:

Again, your instincts will probably drive you to take notice of all the countless ads for Life Insurance. It is our instinct for survival (and for the survival of our 'off-spring) that motivates us to take this stuff in the first place.....so you'll likely feel the twinge to do something here.

The thoughts of not having it and 'something happening' is far worse that the thoughts of paying for this insurance. Or at least it is for 50% of the parent population in Ireland anyway - that's the rough % who have Life Cover in place!

If you are wondering 'how much life cover should I have' then by all means you can check out this bad-boy here for an idea of the level that would be sensible, and indeed for the different types that are available to you.

If you are particularly planful and your instincts are kicking your backside you might even start to wonder should you have some form of illness cover or indeed an income protection. These insurances all cost money, nobody likes paying for them, but generally people love the peace of mind they provide and the fact that they quieten the nagging instincts! This episode on Income Protection and this episode on Specified Illness Cover might help a little.

Child-Care:

If you take a scenario (which is by far the most common) where both parents are back to work within 12 months of baby's arrival then the inevitable cost of child-minding will rear it's ugly head! There are obviously scenarios where grandparents etc mind the child and insist on not taking any money for that. Count yourself fiercely lucky if that's the case!!

A local childminder or indeed creche, depending on where you are in the country will cost you anything from €40 to €60 per day. Might not sound a lot, but tally that, averaged at €50 per day, over the course of a month, if it is 5 days per week, and you are at €1080 per calendar month. €12,000 per year. To earn €12,000 as a higher tax earner you need to earn approx €24,000 Gross.

If you are on €60,000 per year that is not far off half of your yearly Gross salary...or in another way nearly every second day you go to work is so that you can pay Childminding costs! Not exactly inspirational stuff I understand, but it is a fact!

Taking Time Out:

This leads nicely to the next aspect we invite you to consider, in advance of baby's arrival. Will you actually want to go back to work after maternity/paternity leave is over? Will you be able to afford not to?

This is the single biggest aspect we would invite new or prospective parents to consider. Aside from the financial cost of reducing hours or indeed of doing no hours of paid work, there is the far more important and fulfilling (we would argue!) aspect of having extended time with your child in their early years.

If you were to take unpaid leave from work would your financial lives fall to pieces? How would the mortgage or rent get paid? How would all other bills be managed? Have you actually looked at the maths yourself? This is essentially what Financial Planning is all about, looking ahead and figuring our what you want to do with your time, as well as with your money! We saw how much of a dent on your salary that Childminding can have....you would obviously be saving yourself that chunk if you were not working and were doing that yourself!

If your married couple have only one earned income between them, as of January 2018, that household will be able to earn €43,550 before being hit with the higher rate of tax. In essence what this means is that the effective rate of tax on the household income would obviously be less if only 1 person is earning an income, meaning the 'worker' would find they take home more Net Income if the other spouse takes time out.

Taking time out is not obviously a necessity, it is a choice. We invite you to consider if this is a likely choice you want to make, and to plan for it if it is something you aim to do.

Long Term (6 years and beyond!):

Aside from feeding a growing child, and aside from everything above and the usual clothing, social, sport and other expenses the most commonly thought-about is Education. While the expenses of National and Secondary school appear mostly manageable to working parents, it is the looming 3rd level education which causes most parents to squirm!

We have covered it before, the most common ways to prepare for the costs of college fees. Indeed it was such a big subject matter that we had to split it into 2 parts, Part 1 & Part 2!

If you have young kids at this stage you might feel that College fees are a long way away, and you'd be right. Having said that unless you have the money already set aside for it (€11k per year per child) now might be a good time to start figuring out how you are going to pay for it all!

Nonesense:

As much as we love the topics we cover here, and sharing ideas with like-minded people to help them manage their money the idea that you will or won't have kids based on the financial aspects is a little 'off' if you ask us. Yes it is prudent to be prepared and planful but for those of us who are lucky enough to be able to have and care for their own child it is our primal instinct to create and give another being the chance to live a fulfilled and fun-filled life.....money is unlikely to come into that debate....it may, but it will unlikey be the decider! So take all of these articles about the financials of kids with a pinch of salt, take what nuggets you like from them, but please don't let it scare you, you'l be awesome!!

Thanks a mill for reading (and sharing). We'd love you have you join our community.

Paddy Delaney

QFA | RPA | APA | Qualified Coach

This week we take on a subject which, while not that earth-movingly exciting, has gained in popularity over recent years in the investment industry, and that subject is rebalancing.

Rebalancing, in the simplest and most honest terms can be described as taking money out of your 'winners' and putting it into your 'losers'! Please bear with us and we'll explain!

With lots of lovely head-lines lately talking about Equities at all-time highs and general euphoria about investing.......it might (or might not pay) to be aware of rebalancing, and how it impacts on your investments.

When it comes to Investing & Pension Funds in Ireland in 2017 or indeed most aspects of creating investment portfolios, since 2008 there has been a sharp focus on ensuring that investments are well diversified. Due to the scorchingly severe falls in values of equities and property at that time people have been once bitten and are now twice shy. There is now a big push to diversify between different asset classes to reduce that volatility & who'd blame them.....even though it this does fly in the face of the fact that a broadly held basket of equities outperforms any other asset class over the long term!

Product providers and indeed the industry at large now go to great lengths to encourage people to avoid being overly exposed to one particular asset (even if, as already stated, historically one particular asset class has performed above all others!). Investors are now encouraged to have a balance of 2 or more asset classes, such as equities and bonds, or equities, bonds and property etc etc. This is done ultimately in order to try reduce the volatility yet still achieve reasonable returns. For more on diversification by all means this might be useful (or not!).

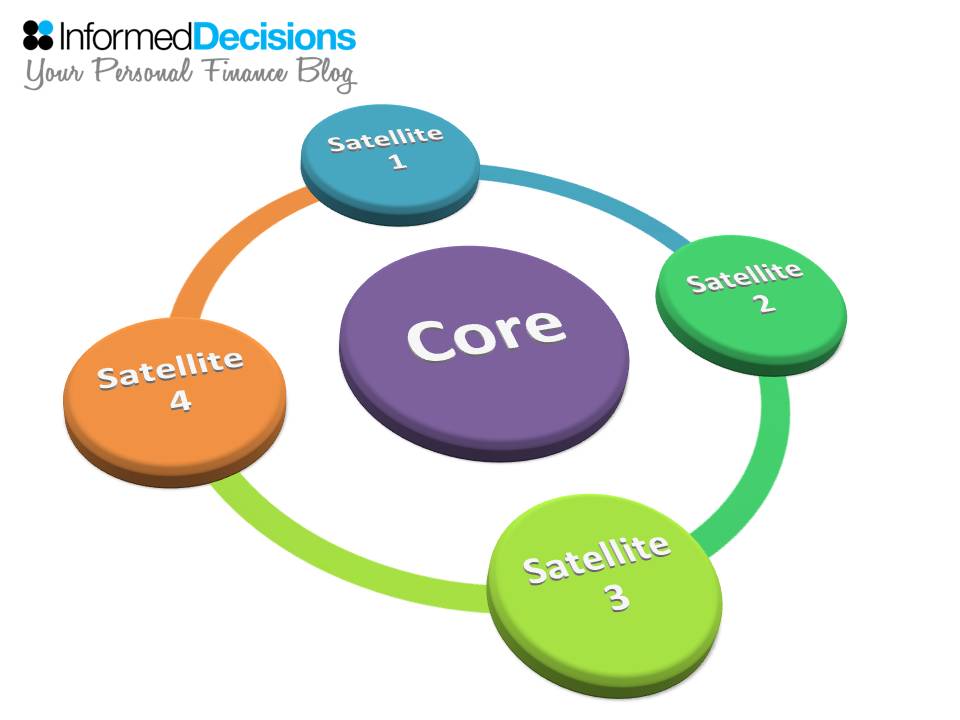

What is Rebalancing?..............by all means check out our blog version of this episode.....here.

While it might sound a little like a project to build the next NASA space-rocket this is a fairly simple investment approach that Irish investors have access to, so strap yourself in! Before we begin may I outline that the word 'satellite' is one of those words that I really struggle how to spell.....for some reason I keep typing it as 'satelitte'.......so this particular blog might take me a while to get done!!

Anyway, here we will take on the task of sharing ideas with you keen investors on the concept of 'core-satellite' investment portfolios, how to approach it, what to watch out for and ultimately outline the pros and cons of this particular approach. Lovely-jubbly. Core Satellite investment in Ireland will never be the same again!!

What is a Core-Satellite Portfolio?

Core-Satellite is not something you might hear often here in Ireland, however elsewhere in the world, such as US & UK, it is a very well established and indeed popular approach to take to investing your funds.

Ultimately this approach aims to blend the 'best of both worlds', by combining both Passive and Active strategies into the one portfolio. There has been long term debate over which strategy is best for investors. A recent well documented event was Warren Buffet winning a 10 year, 1-million dollar bet with a hedge fund manager that a passive fund would beat an actively managed hedge-fund over 10 years from 2008. To date the passive fund has delivered over 7% while the hedge fund has delivered just over 2%........it was a land-slide. Yet there are periods where an active fund manager has outperformed passive and indeed been able to reduce volatility levels at certain times and in certain markets. Find out a little more about active strategy in our hugely popular interview with Will Spark here.

As a result of this ongoing debate people who are unsure of the long-term best option for them can avail of a 'bit of both' styled approach. That is where core-satellite comes into play, and satisfies that need.

How To Build A Core-Satellite Portfolio?

A portfolio is just a fancy way of saying, 'a mix of investments/holding'. Its one of these words that sounds nonce, it's straight-forward however! You can create a portfolio with a trusted advisor (our default recommendation!) or you can build one yourself and attempt to manage it over the years directly with an investment firm or online trading. You simply purchase the appropriate funds/holdings and re-balance it each year or so (we'll have an episode on what re-balancing is all about very soon!).

Provided you have set up your portfolio (mix of stuff!) in line with your appetite and tolerance for volatility and indeed your long term objective there is no need to ever alter the portfolio. If your long term plan doesn't change then there really is no need to change the mix.

In any core-satellite portfolio there will be a certain percentage in Active and a certain percentage in Passive. The core will naturally form the basis of the portfolio, while the satellite represents the add-ons to the core.

What To Watch Out For?

The split should be based on a number of considerations, including but not limited to the following:

Investor tolerance for volatility

Ability to identify top performing and low-cost Active Managers

% Return needed to achieve the end goal of investor

There are many who would argue that Passive holdings such as Index Funds should form the basis of the core, that historically this offers the greatest return over the long term relative to the risk and volatility. The satellites should be a combination or small selection of managed funds, to offer diversification from the core and a potential to offer growth/stability/selection in preferred investments. Unless you or indeed your trusted advisor are skilled at identifying low cost and high performing Active holdings then it may be a case that having these smaller holdings in your satellites might make some sense.

Others would argue that the Core should be more boring and less volatile investments (holdings), where it is risk-managed and relatively steady, in order to try deliver a certain expected long term return. This would offer scope to go for more exciting and volatile satellites to attempt to drive performance upward. This would, or indeed should, lend itself to more predicable returns over the long term, albeit likely to deliver less return than the above example.

We've said it before and we'll say it again, begin the construction of your portfolio with the end in mind....what is the objective of it, what are you aiming to achieve, what are you willing to accept in terms of volatility in order to achieve it. The questions, or more-so the answers, should be a large determinant in building and choosing the percentages in each.

As a general guideline if an investor is building a core-satellite portfolio typically the core would represent at least 50% of the overall value, the remainder split between one or many satellite holdings.

If you are into Financial Planning and want to be more mindful in your investments then the idea of investing with a particular investment philosophy and plan is a must....otherwise it is purely investing for the sake of it...and that usually doesn't end well!

Irrespective of whether it is Active or Passive it always pays to be aware of the costs of the funds, getting access to the Total Expense Ratio (TER) or the Ongoing Charges Figure (OCF). For more on the impact of fees on investment growth go here.

Pros & Cons:

In short the pros are that it allows you access to both Passive and Active in a structured manner within a single investment portfolio. It makes it easier to monitor your split between the two strategies and to therefore re-balance it each year to keep it in line with how you initially set it up.

Some of the cons one would see are that it can be difficult to keep a clear line of sight on the overall portfolio it if there are many smaller satellites. It can therefore also tempt an investor to make changes to the portfolio selling and buying satellites irrationally, which more often than not will have a negative impact on it's long term performance.

Bottom-Line:

Core Satellite is a form of portfolio investing. If you are interested in a blend of Active and Passive this approach can make a lot of sense. If you are strongly biased toward either then it can also be a sensible approach to still keep an element of the one you less favour, as always it can add another level of diversification to the portfolio and offer growth/risk-management depending on the blend you opt for.

If this is new to you you may well now think that Core-Satellite seem like a complex sounding name for a fairly straight-forward approach, and you'd be right, it is! However the clearest benefit from our perspective is that it provides a structure around which to build a sensibly constructed portfolio.

Thanks for checking out this episode, and by all means we'd love you to join our growing community of 'informed-decisioners' over here!

Thanks for sharing.....

You're a legend!

Paddy

QFA | RPA | APA | Qualified Coach

It is the first thing people ask when they hear you work in the space of helping people manage money.....'What should I invest in?'. The only appropriate answer to that question, I believe is along the lines of 'it depends on what your objective is'. This answer usually isn't what they expect, they expect a pitch for a certain share or investment in a German Shopping Centre Fund!

The next question that follows will usually be....'How long should I invest for'? That is the question we are here to discuss. And for once I have had the time to write a short piece, so enjoy!!

Firstly, and as always, we are chuffed that you have checked out our website & podcast. We are on a mission to help Ireland's normal folk to make the most of their financial lives and make Financial Planning accessible to all. We ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

As always we're totally upfront when we say that we are openly biased on this little topic!.....We believe it is a simple concept that costs nothing and that no other tool, process or approach will have as significant an impact on your ability to be a consistently successful investor, as time.

How Long Should I Invest For?

This is a non-question, deserved of a non-answer! If you are really beginning with the end in mind you will know how long you plan to invest for, you will know why you want to invest and with the assistance of a true financial advisor will know what level of return you need to achieve to ensure you meet your goals. But forgiving that let's looks briefly at the 3 timeframes which might be considered 'normal'.....

If you are constrained to an investment shorter than 5 years and you wish to invest in anything like Equities or Property funds then you are absolutely gambling. Best of Luck!

If you are in a position to invest for between 5-15 years then you are in reasonably positive shape for making a success of it, not quite a thoroughbred of investment but pretty close!

If you are open to and indeed fully committed to investing, and leaving it invested for 20 years or more then you are, if over 100 years of history is anything to go by, as close to a bookies 'cert' as is statistically possible!

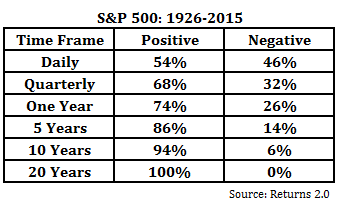

What Does History Tell Us?

Well interestingly enough you will see from below chart that on any given day the great companies of the USA (The S&P 500) are a coin-toss as to whether they will be up or down. It is this fluctuation that all those media articles, blog posts & Bloomberg-esque TV programmes feed on on a daily basis. But sure what possible difference does that make to the a 20 year investment plan? None.

If you invest for any 12 month period you are more likely to end up than down. However if you invest over a 15 year period you would expect to experience a negative return once in every 500 rolling periods. The return would be positive 499 times and negative once!

Over a 20 year period, it has not had a single 20 year rolling period (with a new period starting every month) there has never been a single period where the return has been negative.

Speaking of 20 year periods, the worst 20 year return was 54%, however the worst 30 year return was 854%!

We can deny it, dissect it, counter it and challenge it all day long, however the fact of the matter is that these are facts, and facts we don't often hear. My guess is that it is because there are lots of advisors selling products, with no awareness whatsoever of the actual market and historical facts.

Where Do People Go Wrong With Investment Durations?

It is a natural instinct to keep a hold of accessible cash, quite right. Indeed it'd be tantamount to madness to invest money into a similar asset as above without having a 'stash' that they could access for short-term needs or emergencies.

Outside of that however it is tantamount to madness to not preserve the purchasing power of your money and to leave it on Bonds or Deposit for the long term irrespective, of your age.

One of the core problems I see is that many investment funds accessible to Irish investors have recommended or indeed minimum time-frames. These are usually 5 to 7 years, and set as a result of product constraints or need to extract enough fees to cover the cost of selling that product to the investor! Unfortunately this timeframe can now become the target, to leave it there for the 5 years and then take it out. No No No!

If you are indeed entering the investment with a plan, with clarity on the return you want to achieve and the outcome you are aiming for, please don't have 5 years as your target, give yourself a much higher probability of success and 'go long'.

If you did find this useful please share, love it to bits and send me an email saying why...if you thought it was rubbish please send me an email and tell me why!

Thanks!

Paddy Delaney

QFA | RPA | APA | Qualified Coach

There are many many people today in Ireland pining for their own home, looking to get onto the property ladder, sick of paying rent or perhaps living with parents or family. There are usually a one or more of the following barriers to them doing so; cannot get a mortgage large enough, cannot find a suitable home in the location they want, or they are waiting for the 'next property crash' before buying.

This last barrier is an interesting one, and indeed one which many many people of our generation are asking themselves; should I wait for a property crash instead of buying a house now. Recent property price increases are well documented, as are the issue around supply etc....we are not here to discuss these. What we are aiming to do is separate the financial from the emotional when it comes to these decisions.....because let's face it, whether we realise it or not that is often the dilemma!

How Do Property Prices Compare To 'The Peak'?

How prices compare to the past is a non issue, it is not a determinant or a predictor of any future event. However this is ultimately what is encouraging people to sit and wait for the crash......it's the recency of the property crash of 2008-2013, where prices of houses fell on average of 55%. With this so recent in memories one could not at all be blamed for being keen to avoid such a burning again. Let's face it who would volunteer to pay €300,000 for something only for it to be worth €140,000 five years later....!

A typical 3 Bed-Semi in County Meath in Jan 2007 was in the region of €315,000 (knowing from personal experience!). Those same houses fell in value to approximately €140,000 by 2013, after which point they begun to increase in value.....currently standing at around €260,000.

Similar value fluctuations can be seen right across the country, falls of 55% over 5 years and then increases (from that low point of approximately 60-70%), but they are generally not back to the 2007 level, despite media coverage stating that they are. So does that mean you should wait until they hit the next peak, let them fall and then buy?? Lets see what would need to happen...

Wishing For Armageddon?

So you and your partner have two decent incomes, both in steady jobs, have been saving €800-1,500 per month for the past few years, have €40-€50,000 squirreled away in a savings account with your bank or credit union..........you have observed the price of property rise in the region of €2,000 per month, and you are saying to yourself 'here comes the boom'! With that mindset, you will hold and hold until the next 'correction' comes.....when will that be?

Nobody knows, it could be 5 years, it could be 10 years, it could be 15 years.....and how much will prices fall? Could be 10%, could be 25%, could be 50%, nobody knows! The bottom line is that if you are waiting (and therefore hoping) for prices to fall in the region of 30-50%, the fact is that this may never happen. You may well find that you are still saving in 10 years time, you might have €200,000 built up, but then again the price of that €280,000 house in 2017 may be €520,000 in 2027! Do you buy then??

We are all in favour of beginning with the end in mind here. What have property prices done over the long term? The long term growth rates of property value, as captured by Ronan Lyons in a study of a few years ago showed that prices increase at an annual inflation adjusted rate of 2-5%, and no more, on average.

What Would Have To Happen For Prices To Fall 50%??

This is an interesting one. If you are that couple with a nest egg of savings waiting for the next property crash it's worth considering what that might look like! And while we are not economists here at Informed Decisions, we do believe that if property prices are to drop by 50% it will impact more than just property.

Look back on 2008-2013. Without getting too dramatic about it unemployment rate rocketed from 4% to 15%. Many decent folk just like you lost their jobs and their incomes fell to nothing. There were very few jobs out there unless you were super skilled in certain technical roles. There was catastrophic problems with the financial system, taxes increased on those who were working and large shortfalls in government cash-flows needed to be plugged by Europe.

The impact of this and indeed many other factors was that banks essentially stopped lending! When they did lend it was only to the most 'gold-plated' of customers, those with impeccable savings, employment and credit records....they didn't lend to you if your job was in jeopardy or indeed gone!

While not suggesting that you as an individual would lose your job if property prices fell dramatically in the future, it is realistic to expect a potential impact on income, and indeed on the ability to borrow what can now be borrowed. For instance a couple with combined incomes of €110,000 could expect to be able to borrow in the region of €400,000 (based on the salary only and nothing else). If there was another major 'correction' would that €400k be borrow-able.....who knows!

Worst Case Scenario:

So if you are in the position where you are ready to go, and are holding off for Armageddon to strike and prices to plummet. Other than the possibility of your dreams not coming through, lets say you decided to buy a home now. Imagine you borrowed €315,000 and bought that house for €350,000 (90% mortgage!). Property prices grew by 5% per annum for the next five years. In 5 years time your property is worth €440,000! Happy Days!

Lets assume Armageddon hit in 5 years time - that's a random selection not a prediction!! Over the following 3 years prices fall by 50% nationwide. The economy is in a spin, everyone is saying 'this is the end of the world!'.

Absolute disaster?? Your house fell from €440k to €220k over those 3 years. At this point, 8 years into the term, your mortgage balance is €256,000! Yes it's negative equity but so-the-hell-what!!! Does that negative equity have any impact whatsoever on your lifestyle or indeed on your financial wellbeing? It may indeed feel bad, nobody likes to be repaying a loan on something that is more than it's value. But other than that emotional aspect it has no bearing on your financial position.

It is only if you needed to sell it would be an issue. In addition we have seen since 2013 how the price of property can recover over a 4 year period given the right circumstances. Prices have almost doubled from the low point of 2013......meaning that in the above scenario the property would increase in value from the low of €220,000 back up to €440k territory, and by that stage (12 years in) your mortgage would be approximately €220,000!

If prices didn't recover, assuming you continued to be able to repay your mortgage you would be out of negative equity within that 12 year time-frame.

Separate The Financial From The Emotional:

While we do hope we have outlined the above fictitious scenario in some sort of clear manner it may all still seem a baffling consideration to make! Financially speaking buying a house is a gamble, no 2-ways about it.....you are making a huge investment at a particular point in the market. If you were an investor I would be advising you to insist on huge diversification not to invest 100% into one thing, not possible when buying a home unfortunately! Whether the point you buy-in is high or low relative to the future prices nobody knows, and that is a fact.

Emotionally it is often a solid investment. You want to put down roots, you want to be able to call it your own, you want to be able to have a 'roof over your head' that you own (theoretically anyway!).

If you can financially handle the potential armageddon, and emotionally you think you could stand up to it then it may well make sense to you to commit to your new home.

We hope this provided food for thought. As someone who previously bought at a peak we understand how it can feel, and whether or not it financially impacts. Our aim is that this piece will hopefully help you indeed a loved-one....so please do share the love!

Thanks,

Paddy Delaney

QFA | RPA | APA | Qualified Coach

It's Showtime!

If you swim too close to a shark it'll bite ya! If you have decent savings, investments and pensions you could be in danger of getting bitten too! We're here to help you understand if you are in danger of getting bitten, it's up to you as to whether to stay in that water or not!

We are realists here at Informed Decisions and so no matter what you get done; a tap fixed, a wall painted, a tooth pulled, a will administered, a house bought or indeed an investment invested you will pay a price for those services! This episode it aimed squarely at ensuring you know the impact of any fees you are paying on your financial products, wealth management or indeed retail investment products here in Ireland. We'll also share some insights on what you might be able to do to help yourself avoid a nibbling......because ultimately controlling your costs is a smart thing to do!

Firstly, and as always, we are chuffed that you have checked out our website & podcast, and we ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

Click here to access the full show notes version.

Thanks for listening & sharing!

Paddy Delaney.

QFA | RPA | APA | Qualified Coach

Thanks for tuning in to this weeks' Episode, our 52nd, and Informed Decisions' 1 year anniversary!!

We bring you something pretty special, interviewing one of Ireland's brightest talents in regards Investment Management, Will Sparks.

Will tells it like it is, so it was a pleasure to have him on the show, and in addition to that he knows how to manage investments....who better to help identify some insights for our listeners!

By all means please do visit our small website, and check out all our podcasts and blogs, and if you like what you see we'd be delighted to have you join our mailing group!

Thanks all.

Paddy Delaney

Creator & Dogsbody @ Informed Decisions!

QFA | RPA | APA | Qualified Coach

Hey!

In a recent blog we took a look at the big 6 risks which exist when it comes to managing ourselves and our money. We had everything from ostrich risk (sticking our head in the sand!) to longevity risk (living too long!).

This time around we are going to focus on practical tools we can apply to our money and savings, in order to ultimately have a more pleasant investment journey, the growth we expect, and the appropriate outcomes......please keep reading!

As we try do things slightly differently here at Informed Decisions we are going to attempt to explain all this using the metaphor of a plane journey to New York.....chocks away!

Before we fly off into the blue yonder, if you enjoy this blog, all we ask in return is to help us spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! We are on a mission to make Investing and Financial Planning here in Ireland a doddle! Be delighted if you checked out our why.

What is Investment Risk?

Some say (indeed the 'Economic Times') that it is the probability or likelihood of occurrence of losses relative to the expected return on any particular investment.

In plain english therefore we can take it as the risk of your investments not doing what you expected or indeed hoped. Comparing it to a flight it's like (I would use the work akin but it sounds horrid pretentious no!?) getting on a flight from Dublin heading for New York to do a huge shopping spree but ending up in Mexico! You expect one thing but get another, and you may not be that happy about it!

Hey all, in this 50th episode of the Informed Decisions Financial Planning Podcast we will aim to share insights on the very best mortgage that you can get here in Ireland; whether you are aiming for your first mortgage or have a collection of them we hope to share ideas which will save you a small fortune over your life-time. We also have a short guest appearance from Seamus & Conn (future Informed Decisioners!!)....

All we ask in return is to help us spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

We shared insights a number of months ago in what still remains one of our most popular blogs in the area of over-paying one's mortgage and the impact that has on the number of years you will be lumbered with it and also the lump of interest you would have paid.

Speaking of which, if I was to offer you €38,000 of a saving over the next 20 years, and all you had to do to earn it was about 8 hours of work, and an initial outlay of €1,000 to €1,500 for solicitor fees......what would you do? Many of us might fall into the most irrational behavioural finance phenomenon and not be able to see past the cost of €1,500, but on the face of it there surely is no doubt that we know it makes financial sense, right??

Take a listen to find out what we are talking about this week!

Thanks a mill.

Paddy Delaney

QFA | RPA | APA | Qualified Coach

We are joined by Professional Coach Niall English, to uncover exactly what coaching is, how it can be of benefit to us in achieving the things we want to achieve.

We also take a look at how it might be useful if you find yourself in need of making some changes to your finances. Here at the home of unbiased financial planning in Ireland we like to bring some fresh ideas.....this is our latest!

Plus, Niall shares some practical tools we can all use in order to make some real improvements in regards to our finances.

Hopefully you enjoy!

If you do then please share, join our community and spread the word!

Thanks a mill.

Paddy Delaney

QFA | RPA | APA | Qualified Coach