It is the first thing people ask when they hear you work in the space of helping people manage money.....'What should I invest in?'. The only appropriate answer to that question, I believe is along the lines of 'it depends on what your objective is'. This answer usually isn't what they expect, they expect a pitch for a certain share or investment in a German Shopping Centre Fund!

The next question that follows will usually be....'How long should I invest for'? That is the question we are here to discuss. And for once I have had the time to write a short piece, so enjoy!!

Firstly, and as always, we are chuffed that you have checked out our website & podcast. We are on a mission to help Ireland's normal folk to make the most of their financial lives and make Financial Planning accessible to all. We ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

As always we're totally upfront when we say that we are openly biased on this little topic!.....We believe it is a simple concept that costs nothing and that no other tool, process or approach will have as significant an impact on your ability to be a consistently successful investor, as time.

How Long Should I Invest For?

This is a non-question, deserved of a non-answer! If you are really beginning with the end in mind you will know how long you plan to invest for, you will know why you want to invest and with the assistance of a true financial advisor will know what level of return you need to achieve to ensure you meet your goals. But forgiving that let's looks briefly at the 3 timeframes which might be considered 'normal'.....

If you are constrained to an investment shorter than 5 years and you wish to invest in anything like Equities or Property funds then you are absolutely gambling. Best of Luck!

If you are in a position to invest for between 5-15 years then you are in reasonably positive shape for making a success of it, not quite a thoroughbred of investment but pretty close!

If you are open to and indeed fully committed to investing, and leaving it invested for 20 years or more then you are, if over 100 years of history is anything to go by, as close to a bookies 'cert' as is statistically possible!

What Does History Tell Us?

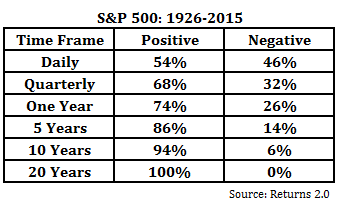

Well interestingly enough you will see from below chart that on any given day the great companies of the USA (The S&P 500) are a coin-toss as to whether they will be up or down. It is this fluctuation that all those media articles, blog posts & Bloomberg-esque TV programmes feed on on a daily basis. But sure what possible difference does that make to the a 20 year investment plan? None.

If you invest for any 12 month period you are more likely to end up than down. However if you invest over a 15 year period you would expect to experience a negative return once in every 500 rolling periods. The return would be positive 499 times and negative once!

Over a 20 year period, it has not had a single 20 year rolling period (with a new period starting every month) there has never been a single period where the return has been negative.

Speaking of 20 year periods, the worst 20 year return was 54%, however the worst 30 year return was 854%!

We can deny it, dissect it, counter it and challenge it all day long, however the fact of the matter is that these are facts, and facts we don't often hear. My guess is that it is because there are lots of advisors selling products, with no awareness whatsoever of the actual market and historical facts.

Where Do People Go Wrong With Investment Durations?

It is a natural instinct to keep a hold of accessible cash, quite right. Indeed it'd be tantamount to madness to invest money into a similar asset as above without having a 'stash' that they could access for short-term needs or emergencies.

Outside of that however it is tantamount to madness to not preserve the purchasing power of your money and to leave it on Bonds or Deposit for the long term irrespective, of your age.

One of the core problems I see is that many investment funds accessible to Irish investors have recommended or indeed minimum time-frames. These are usually 5 to 7 years, and set as a result of product constraints or need to extract enough fees to cover the cost of selling that product to the investor! Unfortunately this timeframe can now become the target, to leave it there for the 5 years and then take it out. No No No!

If you are indeed entering the investment with a plan, with clarity on the return you want to achieve and the outcome you are aiming for, please don't have 5 years as your target, give yourself a much higher probability of success and 'go long'.

If you did find this useful please share, love it to bits and send me an email saying why...if you thought it was rubbish please send me an email and tell me why!

Thanks!

Paddy Delaney

QFA | RPA | APA | Qualified Coach

There are many many people today in Ireland pining for their own home, looking to get onto the property ladder, sick of paying rent or perhaps living with parents or family. There are usually a one or more of the following barriers to them doing so; cannot get a mortgage large enough, cannot find a suitable home in the location they want, or they are waiting for the 'next property crash' before buying.

This last barrier is an interesting one, and indeed one which many many people of our generation are asking themselves; should I wait for a property crash instead of buying a house now. Recent property price increases are well documented, as are the issue around supply etc....we are not here to discuss these. What we are aiming to do is separate the financial from the emotional when it comes to these decisions.....because let's face it, whether we realise it or not that is often the dilemma!

How Do Property Prices Compare To 'The Peak'?

How prices compare to the past is a non issue, it is not a determinant or a predictor of any future event. However this is ultimately what is encouraging people to sit and wait for the crash......it's the recency of the property crash of 2008-2013, where prices of houses fell on average of 55%. With this so recent in memories one could not at all be blamed for being keen to avoid such a burning again. Let's face it who would volunteer to pay €300,000 for something only for it to be worth €140,000 five years later....!

A typical 3 Bed-Semi in County Meath in Jan 2007 was in the region of €315,000 (knowing from personal experience!). Those same houses fell in value to approximately €140,000 by 2013, after which point they begun to increase in value.....currently standing at around €260,000.

Similar value fluctuations can be seen right across the country, falls of 55% over 5 years and then increases (from that low point of approximately 60-70%), but they are generally not back to the 2007 level, despite media coverage stating that they are. So does that mean you should wait until they hit the next peak, let them fall and then buy?? Lets see what would need to happen...

Wishing For Armageddon?

So you and your partner have two decent incomes, both in steady jobs, have been saving €800-1,500 per month for the past few years, have €40-€50,000 squirreled away in a savings account with your bank or credit union..........you have observed the price of property rise in the region of €2,000 per month, and you are saying to yourself 'here comes the boom'! With that mindset, you will hold and hold until the next 'correction' comes.....when will that be?

Nobody knows, it could be 5 years, it could be 10 years, it could be 15 years.....and how much will prices fall? Could be 10%, could be 25%, could be 50%, nobody knows! The bottom line is that if you are waiting (and therefore hoping) for prices to fall in the region of 30-50%, the fact is that this may never happen. You may well find that you are still saving in 10 years time, you might have €200,000 built up, but then again the price of that €280,000 house in 2017 may be €520,000 in 2027! Do you buy then??

We are all in favour of beginning with the end in mind here. What have property prices done over the long term? The long term growth rates of property value, as captured by Ronan Lyons in a study of a few years ago showed that prices increase at an annual inflation adjusted rate of 2-5%, and no more, on average.

What Would Have To Happen For Prices To Fall 50%??

This is an interesting one. If you are that couple with a nest egg of savings waiting for the next property crash it's worth considering what that might look like! And while we are not economists here at Informed Decisions, we do believe that if property prices are to drop by 50% it will impact more than just property.

Look back on 2008-2013. Without getting too dramatic about it unemployment rate rocketed from 4% to 15%. Many decent folk just like you lost their jobs and their incomes fell to nothing. There were very few jobs out there unless you were super skilled in certain technical roles. There was catastrophic problems with the financial system, taxes increased on those who were working and large shortfalls in government cash-flows needed to be plugged by Europe.

The impact of this and indeed many other factors was that banks essentially stopped lending! When they did lend it was only to the most 'gold-plated' of customers, those with impeccable savings, employment and credit records....they didn't lend to you if your job was in jeopardy or indeed gone!

While not suggesting that you as an individual would lose your job if property prices fell dramatically in the future, it is realistic to expect a potential impact on income, and indeed on the ability to borrow what can now be borrowed. For instance a couple with combined incomes of €110,000 could expect to be able to borrow in the region of €400,000 (based on the salary only and nothing else). If there was another major 'correction' would that €400k be borrow-able.....who knows!

Worst Case Scenario:

So if you are in the position where you are ready to go, and are holding off for Armageddon to strike and prices to plummet. Other than the possibility of your dreams not coming through, lets say you decided to buy a home now. Imagine you borrowed €315,000 and bought that house for €350,000 (90% mortgage!). Property prices grew by 5% per annum for the next five years. In 5 years time your property is worth €440,000! Happy Days!

Lets assume Armageddon hit in 5 years time - that's a random selection not a prediction!! Over the following 3 years prices fall by 50% nationwide. The economy is in a spin, everyone is saying 'this is the end of the world!'.

Absolute disaster?? Your house fell from €440k to €220k over those 3 years. At this point, 8 years into the term, your mortgage balance is €256,000! Yes it's negative equity but so-the-hell-what!!! Does that negative equity have any impact whatsoever on your lifestyle or indeed on your financial wellbeing? It may indeed feel bad, nobody likes to be repaying a loan on something that is more than it's value. But other than that emotional aspect it has no bearing on your financial position.

It is only if you needed to sell it would be an issue. In addition we have seen since 2013 how the price of property can recover over a 4 year period given the right circumstances. Prices have almost doubled from the low point of 2013......meaning that in the above scenario the property would increase in value from the low of €220,000 back up to €440k territory, and by that stage (12 years in) your mortgage would be approximately €220,000!

If prices didn't recover, assuming you continued to be able to repay your mortgage you would be out of negative equity within that 12 year time-frame.

Separate The Financial From The Emotional:

While we do hope we have outlined the above fictitious scenario in some sort of clear manner it may all still seem a baffling consideration to make! Financially speaking buying a house is a gamble, no 2-ways about it.....you are making a huge investment at a particular point in the market. If you were an investor I would be advising you to insist on huge diversification not to invest 100% into one thing, not possible when buying a home unfortunately! Whether the point you buy-in is high or low relative to the future prices nobody knows, and that is a fact.

Emotionally it is often a solid investment. You want to put down roots, you want to be able to call it your own, you want to be able to have a 'roof over your head' that you own (theoretically anyway!).

If you can financially handle the potential armageddon, and emotionally you think you could stand up to it then it may well make sense to you to commit to your new home.

We hope this provided food for thought. As someone who previously bought at a peak we understand how it can feel, and whether or not it financially impacts. Our aim is that this piece will hopefully help you indeed a loved-one....so please do share the love!

Thanks,

Paddy Delaney

QFA | RPA | APA | Qualified Coach

It's Showtime!

If you swim too close to a shark it'll bite ya! If you have decent savings, investments and pensions you could be in danger of getting bitten too! We're here to help you understand if you are in danger of getting bitten, it's up to you as to whether to stay in that water or not!

We are realists here at Informed Decisions and so no matter what you get done; a tap fixed, a wall painted, a tooth pulled, a will administered, a house bought or indeed an investment invested you will pay a price for those services! This episode it aimed squarely at ensuring you know the impact of any fees you are paying on your financial products, wealth management or indeed retail investment products here in Ireland. We'll also share some insights on what you might be able to do to help yourself avoid a nibbling......because ultimately controlling your costs is a smart thing to do!

Firstly, and as always, we are chuffed that you have checked out our website & podcast, and we ask for your help to spread the word, share the article with the little icons at the bottom, check out the podcast, and in general just be a huge fan of our little site! Be delighted if you checked out our why.

Click here to access the full show notes version.

Thanks for listening & sharing!

Paddy Delaney.

QFA | RPA | APA | Qualified Coach